The Black Box Bank

Banks Are Becoming Smarter, Faster and More Profitable. But Who Remains Responsible?

For generations, banks were among the most visible institutions in society. Customers walked into local branches. Financial decisions involved conversations. Problems could be discussed with employees who understood local communities and individual circumstances. Banking was not always fast or efficient, but it was visible. People generally understood where decisions were made and who was responsible for them. Today that visibility is gradually disappearing.

Across the financial sector, banks are rapidly adopting artificial intelligence, automation and algorithmic decision-making. Payments happen instantly. Fraud detection is increasingly automated. Customer interactions are shifting towards digital channels. Internal processes are increasingly supported by AI systems.

In itself, none of this is surprising. Technology has always transformed banking. What is striking, however, is how little public discussion exists about what may be lost in the process.

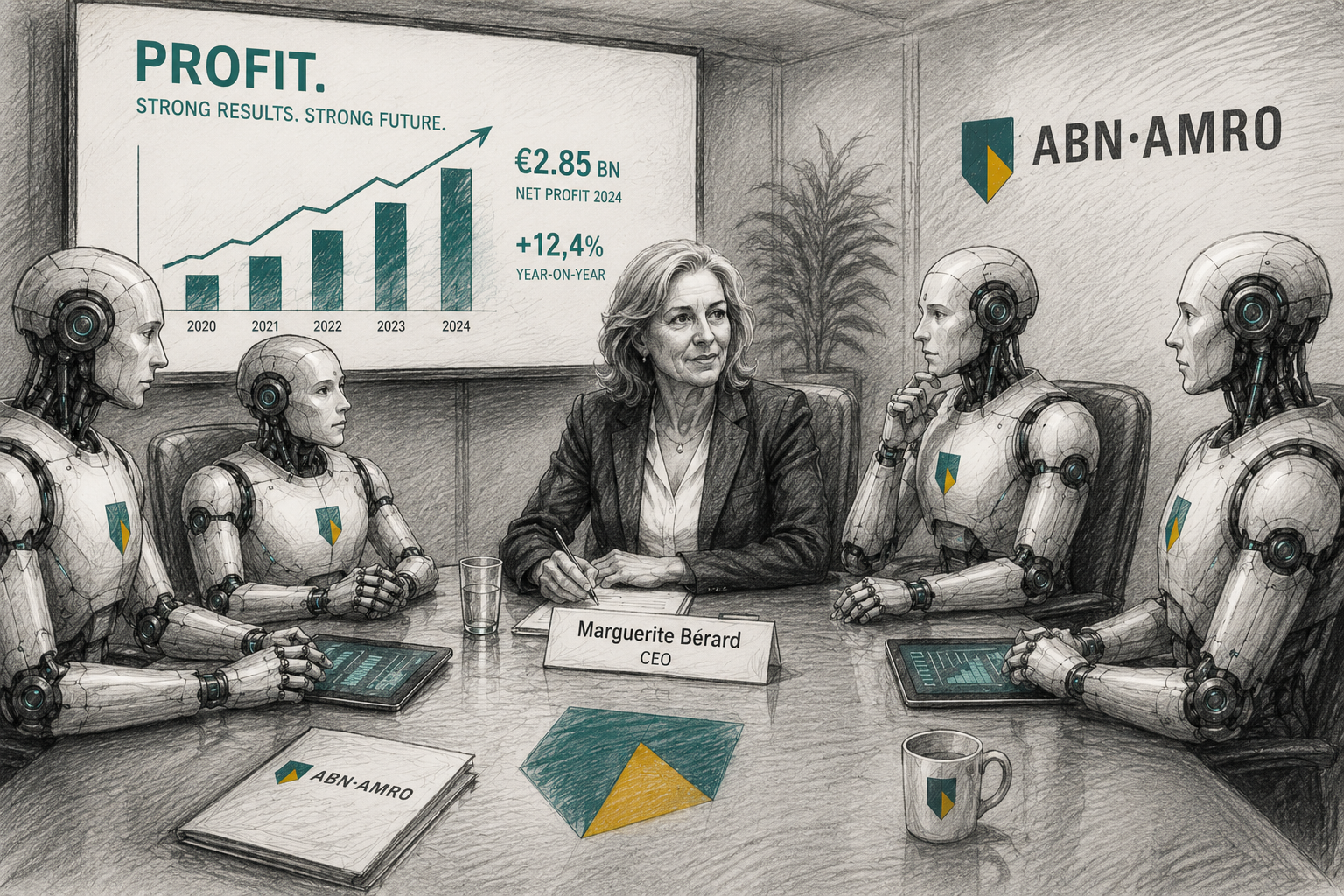

Recent statements from ABN AMRO offer an interesting glimpse into this transformation. The bank has publicly highlighted that approximately 85 percent of its employees are now using AI tools in their work, while simultaneously reporting strong financial results and continued efficiency gains.

For investors, this sounds like a success story. Higher productivity. Lower costs.Stronger profitability. Yet the announcement also raises a broader question that extends far beyond a single institution.

If banks increasingly communicate their progress in artificial intelligence, why do we hear comparatively little about how these technologies affect transparency, accountability and their duty of care towards society?

The New Logic of Banking

For decades, banking relied on a combination of rules and human judgement. Employees could identify unusual situations. Managers could take context into account. Customers could explain circumstances that did not fit neatly into predefined categories.

Algorithms operate differently. They identify patterns. They calculate probabilities. They flag anomalies. They are remarkably effective at scale. But they are also inherently limited.

An algorithm may identify risk. It cannot truly understand vulnerability. An automated monitoring system may detect suspicious behaviour. It cannot easily recognise loneliness, confusion, coercion or manipulation.

The distinction matters because modern banking increasingly affects precisely those citizens who are least capable of navigating complex digital systems.

“The modern bank often knows more about financial risk than it knows about human vulnerability.”

The Disappearing Human Layer

The financial sector often presents digitalisation as a story of convenience. And for many people, it is. Payments are faster. Services are available twenty-four hours a day. Processes that once took days can now be completed within minutes.

Yet every efficiency gain removes a small layer of human interaction. A branch closes. A helpdesk becomes automated. A decision is delegated to a model. A customer is directed to an app.

Each individual change appears minor. Collectively, they transform the relationship between institutions and citizens. The result is a banking system that increasingly resembles a technology platform: efficient, scalable and data-driven, but also more distant.

The paradox is that while banks become increasingly sophisticated at understanding transactions, they often become less capable of understanding circumstances.

From Care Duty to System Duty

Banks occupy a unique position within society. They are not ordinary businesses. They are part of the infrastructure upon which modern economic life depends. Citizens need access to banking in order to receive salaries, pay bills, save money and participate fully in society.

Historically, this special position was reflected in concepts such as duty of care and fiduciary responsibility. Today another responsibility increasingly dominates: protecting the system itself.

Anti-money laundering regulations. Transaction monitoring. Know-your-customer procedures. Sanctions compliance. These functions are essential. No serious observer would argue otherwise.

Yet they also create an important shift. The bank’s attention increasingly focuses on systemic risk rather than human vulnerability.

Financial institutions are becoming exceptionally effective at monitoring transactions. Less clear is whether they are becoming equally effective at protecting vulnerable customers.

This concern is increasingly echoed by consumer organisations, senior citizen associations and debt counselling organisations throughout Europe. They point out that while automated systems are highly aggressive in screening ordinary citizens for compliance, they are often far less effective at protecting those same citizens from sophisticated fraud, social engineering and increasingly AI-assisted scams.

Their criticism is not directed at technology itself. Rather, they question whether banks are investing as much effort into protecting vulnerable customers as they are into protecting regulatory compliance.

The Frictionless Economy

One of the least discussed consequences of digital finance is the disappearance of friction.

Historically, money moved relatively slowly. Transactions involved pauses. Advice could be sought. Questions could be asked. Time existed for reflection. Digital finance removes many of those pauses.

Money moves instantly. Purchases occur with a single click. Credit becomes available almost immediately. Financial decisions that once required deliberation now happen within seconds.

The economic system becomes more efficient. But efficiency is not always the same thing as wisdom. For younger generations especially, money increasingly exists as an abstraction. A number on a screen. A notification. A swipe.

Debt counsellors and social organisations have repeatedly expressed concern that frictionless financial systems can accelerate unhealthy financial behaviour, particularly among younger users. The technology works exactly as intended. That does not automatically mean the social outcome is desirable.

The Transparency Gap

Perhaps the most important issue is transparency. Modern banks know more about their customers than ever before. Transactions. Behavioural patterns. Risk profiles. Financial histories. Digital interactions. At the same time, customers know remarkably little about the systems evaluating them.

When accounts are flagged. When transactions are investigated. When decisions are automated. When fraud occurs. The underlying logic often remains invisible.

When questions arise, institutions frequently point towards privacy obligations, compliance requirements or regulatory constraints.

Sometimes those explanations are entirely justified. Yet they can also create a growing accountability gap, where legal frameworks designed to protect citizens increasingly function as institutional shields against scrutiny.

Victims of fraud may struggle to discover what banks knew and when they knew it. Customers affected by automated decisions are often given outcomes rather than explanations. The underlying logic remains hidden behind a combination of proprietary systems, compliance procedures and legal confidentiality.

The result is a remarkable asymmetry. Banks possess unprecedented visibility into the lives of their customers, while customers possess increasingly limited visibility into the systems evaluating them.

“The defining question is no longer whether banks use artificial intelligence. The defining question is whether citizens can still understand how critical financial decisions are being made.”

Profit, Responsibility and Silence

There is nothing inherently wrong with banks making substantial profits. A healthy banking sector is essential for a healthy economy. Yet a striking imbalance is emerging in how success is communicated.

Financial institutions increasingly publish detailed information about profitability, efficiency improvements and technological transformation. Press releases celebrate productivity gains, AI adoption and shareholder returns.

Far less attention is devoted to questions of duty of care, social responsibility, financial inclusion or the long-term consequences of replacing human judgement with automated systems.

ABN AMRO’s public emphasis on AI adoption illustrates this imbalance. The message is clear: artificial intelligence is improving efficiency and helping to modernise the organisation.

What remains less visible is how the same transformation affects accountability, customer protection and the human dimension of banking.

The result is not merely a technological shift. It is a shift in institutional priorities. And that shift deserves public debate.

The Black Box Bank

This is ultimately not a story about ABN AMRO. Nor is it a story about artificial intelligence. It is a story about the future of institutional trust.

ABN AMRO merely illustrates a broader development occurring throughout the financial sector. Banks are becoming infrastructure. Invisible. Automated. Algorithmic.

For shareholders, this may create efficiency. For institutions, it may create scale. For society, however, a more fundamental question remains.

Who remains responsible when critical decisions increasingly emerge from systems that few citizens can see, understand or challenge? Because banks do more than move money. They help structure participation in modern society.

As banking increasingly disappears behind algorithms, dashboards and automated workflows, transparency itself becomes a public interest.

The future of banking will not be determined solely by how effectively institutions adopt artificial intelligence. It will also be determined by whether they remain willing to explain how that intelligence is used, who remains accountable, and how the human beings behind the data are protected.

Otherwise the greatest risk of the AI era may not be technological failure. It may be the gradual disappearance of visibility, responsibility and trust inside institutions that society cannot afford to lose.

Image Credit

Illustration by Altair Media / OpenAI Image Generation

Caption

As banks increasingly celebrate artificial intelligence, efficiency and profitability, questions about transparency, duty of care and human responsibility risk becoming harder to see.