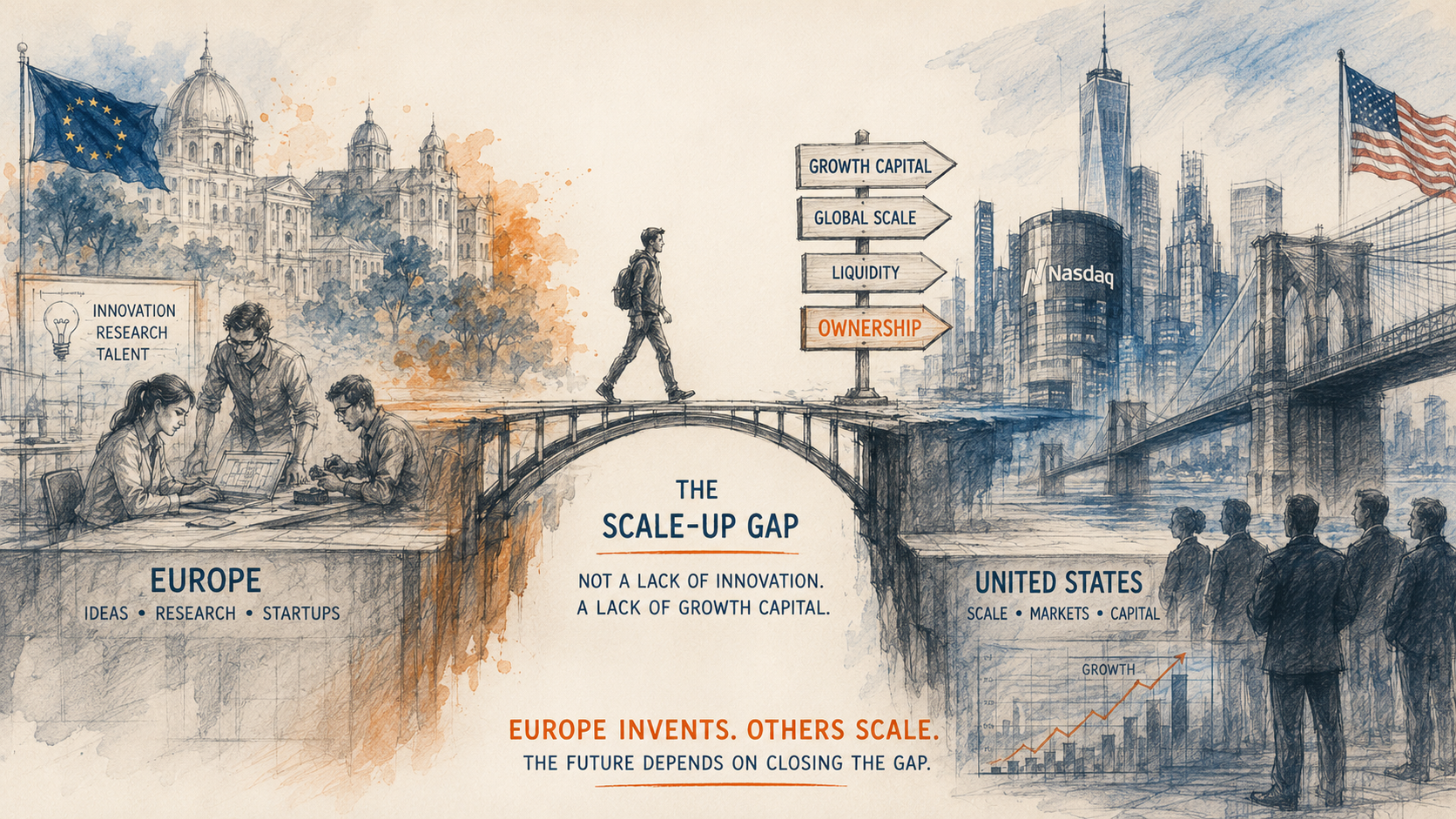

The Scale-Up Gap

Why Europe Invented Companies It Could Not Keep

Europe has long excelled at producing knowledge, talent and technological breakthroughs. Yet many of its most promising companies reach global scale elsewhere. The challenge may not be innovation itself, but the financial architecture required to transform innovation into long-term ownership, influence and economic sovereignty.

Europe has never lacked ideas. Its universities rank among the world’s best. Its laboratories continue to produce breakthroughs in semiconductors, photonics, biotechnology, advanced manufacturing and artificial intelligence. European researchers remain highly cited, while European firms occupy leading positions in industries that increasingly define technological competition. Yet Europe also exhibits a recurring pattern.

Many companies are founded in Europe, developed within European ecosystems and supported by European research programmes, only to mature into global enterprises elsewhere. Their technologies often remain European. Their talent frequently stays in Europe. But ownership structures, stock market listings and strategic decision-making gradually migrate across the Atlantic.

Perhaps Europe has never suffered from an innovation deficit. Perhaps Europe has historically suffered from a growth capital deficit.

The European Paradox

For decades, Europe invested heavily in research and innovation. National governments expanded their scientific capabilities, universities deepened their international networks and European programmes such as Horizon Europe provided billions of euros in funding to emerging technologies. These investments have generated remarkable results.

The challenge, however, rarely appears during the startup phase. It tends to emerge later, when companies attempt to move beyond technological validation and enter a period of rapid international expansion.

At that stage, businesses no longer require millions of euros. They require hundreds of millions, and in some cases billions, to build production capacity, acquire competitors, establish international sales organisations and compete in global markets. It is here that a structural asymmetry becomes visible.

American capital markets have traditionally offered deeper pools of financing, larger institutional investors and a greater willingness to accept risk. Venture capital evolved into a mature industry capable of supporting firms from inception to global scale, while pension funds increasingly became important providers of patient capital. Nasdaq itself developed beyond a stock exchange and became an ecosystem that offers liquidity, visibility, analyst coverage and access to global investors.

Europe, by contrast, often excelled at creating companies while relying upon others to finance their transformation into global champions. Europe produced innovation. America produced valuations. Europe generated knowledge. America captured scale.

The Exit Economy

For many years, this process was not considered problematic. A sale to a major American technology company or a listing on Nasdaq was widely regarded as the ultimate sign of entrepreneurial success. Venture capital firms celebrated successful exits. Founders secured liquidity. Investors generated returns.

From the perspective of individual entrepreneurs, this model often worked exceptionally well. From the perspective of economic architecture, however, it raises more difficult questions.

When ownership migrates, future profits migrate as well. Strategic decision-making shifts elsewhere. Headquarters move. Acquisitions are directed from abroad. The next generation of investments increasingly benefits ecosystems outside Europe.

What appears to be a successful exit for an entrepreneur may simultaneously represent a gradual transfer of economic influence away from Europe.

The distinction between technological excellence and economic ownership therefore becomes increasingly important. Innovation creates capabilities. Ownership determines where value accumulates.

The Capital Question

Europe’s challenge may therefore be less about creating more startups and more about building the financial infrastructure required to retain them. This inevitably brings institutional capital into the discussion.

European pension funds collectively manage some of the largest pools of capital in the world. Yet historically, much of that capital has remained relatively distant from high-growth technology investments. Regulation, prudential frameworks and risk aversion have often encouraged a stronger focus on stability and diversification than on long-term industrial transformation.

At the same time, the United States benefited from decades of institutional investment in emerging sectors, supported not only by venture capital but also by pension funds, public procurement and defence-related innovation programmes. The result is a striking paradox.

Europe possesses world-class research institutions, highly productive industrial clusters and enormous pools of savings, yet it has often struggled to connect these components into a coherent growth ecosystem.

The issue is therefore not necessarily one of scarcity. It may be one of organisation.

A Changing Landscape

There are, however, indications that this architecture is beginning to evolve. Policymakers increasingly speak about economic security, technological resilience and strategic autonomy. Institutional investors are reconsidering their role in supporting long-term European competitiveness, while new investment initiatives seek to provide growth capital for companies that might previously have looked abroad.

Recent multibillion-euro commitments aimed at supporting European scale-ups reflect this broader shift. Such initiatives alone will not eliminate Europe’s scale-up gap, but they do suggest that a different understanding is emerging.

Innovation alone is no longer sufficient. Research creates possibilities. Capital determines where those possibilities ultimately take root.

Perhaps Europe is gradually moving beyond an economic model built around exits and towards one centred upon anchored growth. An economy in which companies are not only founded in Europe, but also scale, mature and remain strategically embedded within European ecosystems.

Ownership as Sovereignty

For decades, ownership was largely viewed as an outcome of market dynamics. Increasingly, it is becoming a strategic variable. Technological sovereignty is difficult to sustain when the ownership of critical companies, the location of their headquarters and the direction of future investment decisions are concentrated elsewhere.

Europe therefore faces a new question. Not simply how to create innovation. But how to ensure that European innovation also becomes European scale, European ownership and European influence. Because perhaps Europe never lacked ideas.

Perhaps it lacked a financial architecture capable of transforming innovation into sovereignty.

Innovation creates capabilities. Ownership determines where those capabilities ultimately reside.

Part of Capital Sovereignty, an Altair Media series examining Europe’s evolving financial architecture, growth ecosystems and long-term economic trajectory.

Credit

Illustration by Altair Media / OpenAI

Caption

The Scale-Up Gap. Europe produces world-class innovation, yet many of its most promising companies reach global scale elsewhere. The challenge may not be invention itself, but the capital architecture required to transform innovation into European ownership, anchored growth and long-term economic sovereignty.